Creating a new credit arrangement

- 10 Aug 2023

- 3 Minutes To Read

- Print

- DarkLight

- PDF

Creating a new credit arrangement

- Updated On 10 Aug 2023

- 3 Minutes To Read

- Print

- DarkLight

- PDF

Article Summary

Share feedback

Thanks for sharing your feedback!

A credit arrangement is the maximum amount a client can take out in loans and overdrafts. It is similar in function to the maximum exposure defined in General Setup > Internal Controls. The main difference is that a credit arrangement can be extended separately and will be different per client, whereas the maximum exposure is a validation that is pre-set at the system level and is the same for all clients.

A client or a group may have multiple credit arrangements, each linked to specific loan and overdraft accounts. Each credit arrangement can have its own constraints, including maximum credit exposure amount and validity dates. The parameters of all loan and overdraft accounts linked to a credit arrangement must be within those constraints.

Mambu has added this functionality to give you additional flexibility in creating credit arrangements by combining multiple accounts, including loan and overdraft accounts, into one agreement.

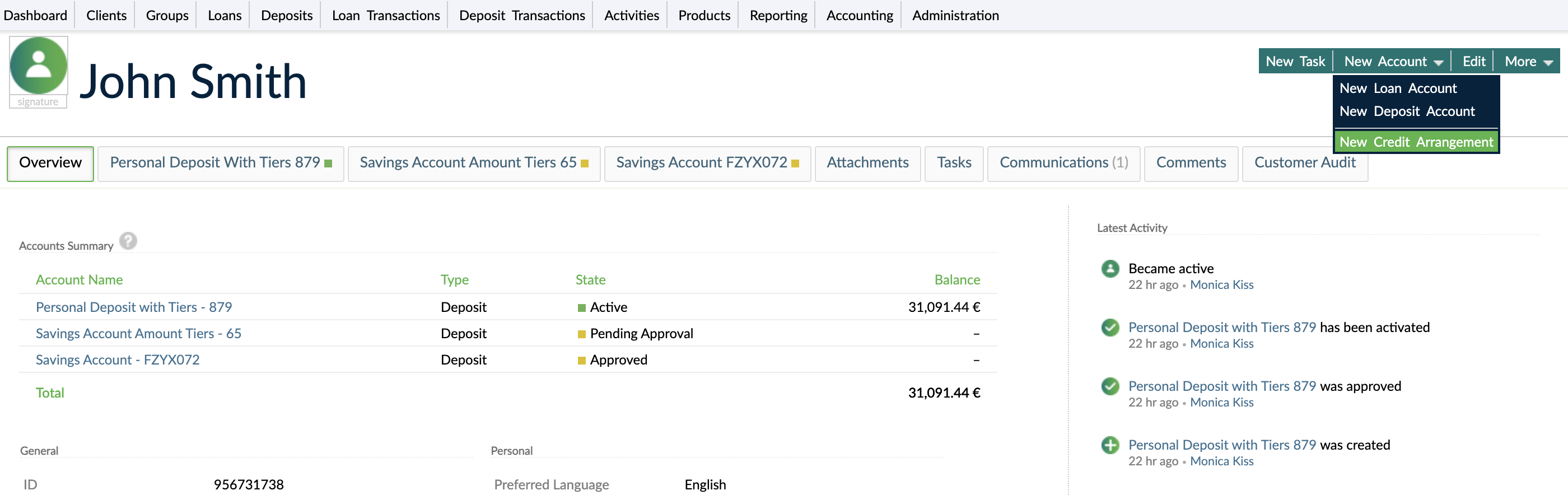

Create a new credit arrangement

Credit arrangements can be defined for each client or group.

To create a new credit arrangement:

- Go to the client or group profile where you want to create a new credit arrangement.

- On the right-hand side of the screen, select New Account > New Credit Arrangement.

- In the Creating a New Credit Arrangement dialog, enter all the required information (more details on this below).

- Select Create Credit Arrangement.

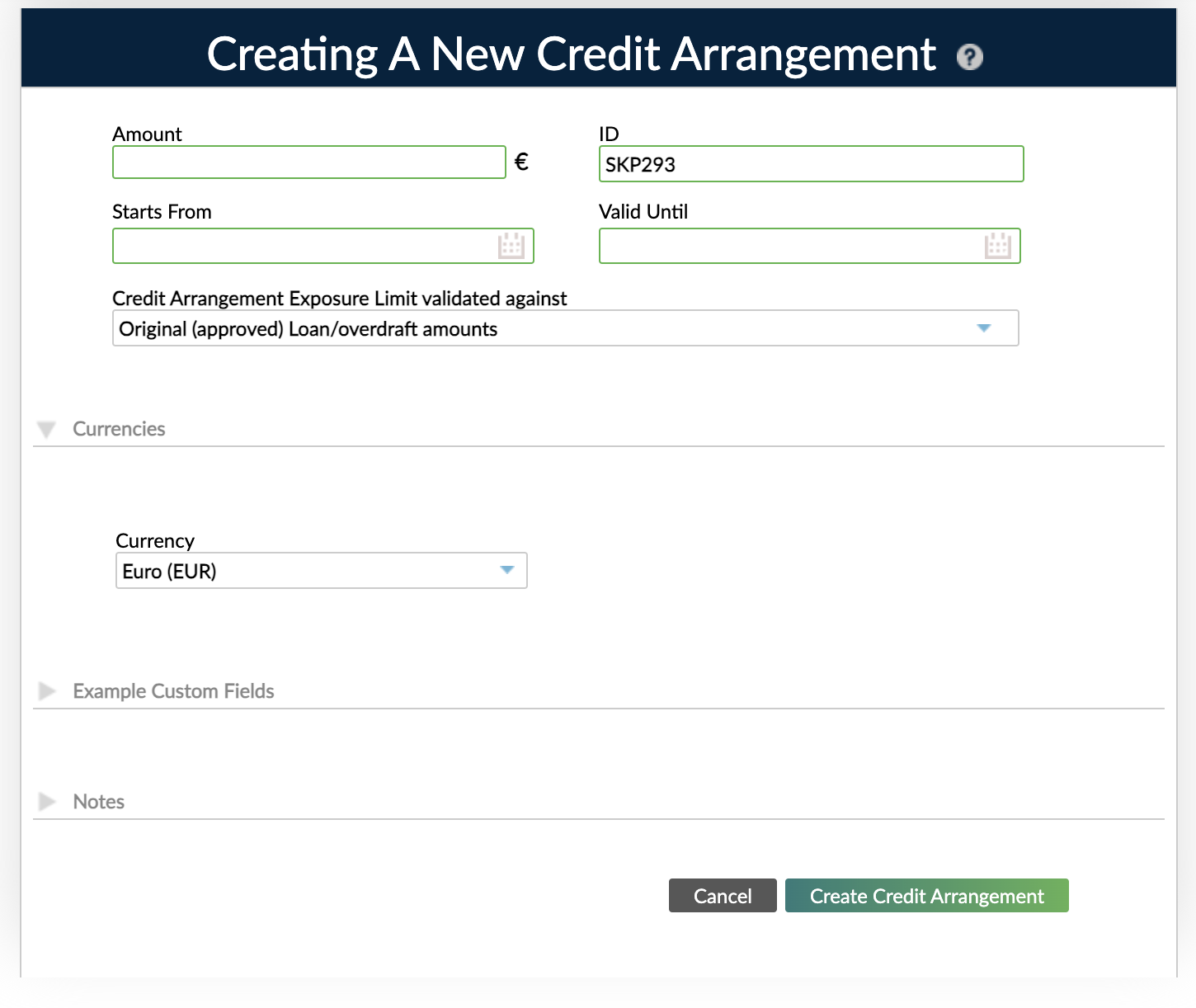

Amount and validity dates

- Amount: The maximum exposure amount.

- ID: Each credit arrangement will be given a unique, automatically generated identifier. The identifier template is predefined at the database level and can only be changed by the Mambu technical team. If you need assistance with this, please contact us through Mambu Support.

- Starts From: Each credit arrangement has a start date and accounts can only be disbursed (loan accounts) or activated (overdraft accounts) after this date.

- Valid Until: Each credit arrangement has an end date and loan accounts can only be disbursed if the expected maturity, as per the schedule, is before this end date. Similarly, overdraft accounts can only be approved or added if the expiry date is before this end date.

- Notes: Include any additional information about the credit arrangement.

Exposure limits

When creating a new credit arrangement, you must select the type of exposure limit against which the credit arrangement will be validated. The options available in the Credit Arrangement Exposure Limit validated against dropdown are:

- Original (approved) loan/overdraft amount: The maximum credit exposure of all loan and overdraft accounts original loan amounts linked to the credit arrangement. The sum of original loan amounts and total overdraft limits may not be in excess of the credit arrangement amount.

- Current (outstanding) loan/overdraft balances: The maximum credit exposure of all loan and overdraft accounts' current balances linked to the credit arrangement. The current outstanding loan/overdraft balance is the sum of all current loan accounts' balances and total overdraft balances.

Loans in Multicurrency

Early Access Feature

If you would like to request early access to this feature, please get in touch with your Mambu Customer Success Manager to discuss your requirements. For more information, see Mambu Release Cycle - Feature Release Status.

If you have the Loans In Multicurrency feature enabled, then you may also define the currency for the credit arrangement. The currencies available will be the ones you have set up for your tenant. For more information, see Currencies.

You will only be able to link loan and overdraft accounts that are in the same currency as the credit arrangement itself.

Get the consolidated schedule of a credit arrangement

You can get the schedule of all the accounts under a credit arrangement, ordered by installment due date, by making a GET request to the /creditarrangements/{creditArrangementId}/schedule endpoint. For more information, see Get schedule in the API reference.

Considerations when using credit arrangements

The following considerations should be kept in mind when handling credit arrangements:

- Clients and groups can have more than one credit arrangement.

- Clients and groups may have some accounts linked to a credit arrangement and at the same time accounts outside of the credit arrangement.

- Only the outstanding funds of the linked accounts are considered in the validations of the credit arrangement exposure limit.

- Each new credit arrangement is given a default ID, which you can change when create or when you edit it.

- Loans with multiple tranches will only have the first tranche dates validated against the credit arrangement constraints, since the other tranches are not firmly confirmed when the account is created.

Was this article helpful?